CA SANJAY DEWAN

Monday, 30 June 2014

| Meetings & Minutes - Changes under the Co.Act, 2013 |

BOARD MEETINGS

1. Time limit prescribed for holding first board meeting. First Board meeting to be held within 30 days of incorporation. [Section 173(1)]

2. Minimum number of meetings to be held in a year:

• For OPC, having more than 1 director, small and dormant Company – 2 [Section 173(5)]

• For all other companies – 4 [Section 173(1)]

3. Time Gap between two board meetings

• For OPC, having more than 1 director, small and dormant Company – Not less than 90 days. [Sec 173(5)]

• For all other companies: Not more than 120 days [Sec 173(1)]

4. Board meetings through video conferencing:

• Directors are permitted to attend board meetings through video conferencing and other audio visual means subject to compliance with the rules in this regard.

• Each director has to attend atleast one meeting in person in a year.

• Presence of director in through video conferencing will be counted for the purpose of quorum.

• Approval of Annual Financial Statements and Board's Report cannot be dealt in a meeting held through video conferencing. [Section 173(1) read with relevant rules]

5. Minimum length of notice for Board Meetings prescribed. Atleast 7 days notice in writing needs to be given to all directors, at their addresses registered with the company, by hand deliver, post or by electronic means. Shorter notice is permitted subject to presence of or ratification by atleast 1 independent director, if any. [Section 173(3)]

6. In case of passing of resolution by circulation, where not less than 1/3rd of the total directors require that a resolution under circulation must be decided at a meeting, the chairperson shall put the resolution to be decided at a meeting of the Board. [Section 175(1) proviso].

7. A resolution passed by circulation needs to be noted at subsequent Board meeting and made part of minutes of such meeting. [Section 175(2)]

8. Matters which cannot be transacted though passing of resolution by circulation:

• to make calls on shareholders in respect of money unpaid on their shares [Section 179]

• to authorise buy-back of securities under Sec 68 [Sec 179]

• to issue securities, including debentures, whether in or outside India [Section 179]

• to borrow monies [Section 179]

• to invest the funds of the company [Section 179]

• to sell investments held by the company (other than trade 5% or more of the paid – up share capital and free reserves of the investee company [Section 179]

• to grant loans or give guarantee or provide security in respect of loans [Section 179]

• to approve quarterly, half yearly and annual financial statements and the Board's report [Section 179]

• to diversify the business of the company [Section 179]

• to commence a new business [Section 179]

• to approve amalgamation, merger or reconstruction [Sec 179]

• to take over a company or acquire a controlling or substantial stake in another company [Section 179]

• to appoint a director in casual vacancy [Section 179]

• to make contribution to a political party [Section 179]

• to appoint or remove key managerial personnel (KMP) and senior management personnel one level below the KMP [Section 179]

• to take on record disclosure of interest by directors and shareholding [Section 179]

• to enter into a joint venture or technical or financial collaboration or any collaboration agreement [Sec 179]

• to adopt common seal [Section 179]

• to appoint internal auditors [Section 179]

• to shift the location of a plant or factory or the registered office [Section 179]

• to accept public deposits and related matters [Section 179]

• to enter into any contract or arrangement with a related party (Section 188)

• to appoint and fix remuneration of a Managing Director / Whole Time Director / Manager [Section 196(4)]

• to appointment a person as Managing Director who is already a Managing Director / Manager of one other company [Section 203(3) Proviso]

• to fill vacancy in the office of any whole time Key Managerial Personnel [Section 203(4)]

• to make loans or investment or give security or guarantee [Section 186(5)]

• to make declaration of solvency in case of voluntary winding up (Section 305)

• to place Register of contracts or arrangements in which directors are interested (Sec 189)

General Meetings

1. All provisions relating to general meetings like length of notice, explanatory statement etc. is applicable to private companies also.

2. First Annual General Meeting should be held within 9 months of closure of first financial year. The provision regarding holding first AGM within 18 months from date of incorporation has been done away with. [Section 96(1)]

3. AGM needs to be held during business hours, i.e. between 9.00 A.M. to 6.00 P.M. on any day that is not a National Holiday. [Section 96(2)]

4. In case AGM has to be called at a shorter notice, consent from 95% of the members is required [Sec 101(1) proviso]

5. Notice of every general meeting needs to be served on every director also. [Section 101(3)]

6. In case of an adjourned meeting, the company shall give not less than 3 days notice to the members either individually or by publishing an advertisement in the newspapers (one in English and one in vernacular language) which is in circulation at the place where the registered office of the company is situated.

7. In explanatory statement, nature of concern or interest of every Key Managerial Personnel and their relatives and relatives of directors also need to be disclosed. If the special business relates to any other company, then shareholding of any director or manager in that other company has to be disclosed if the holding is not less than 2% of paid up capital of the other company. [Section 102]

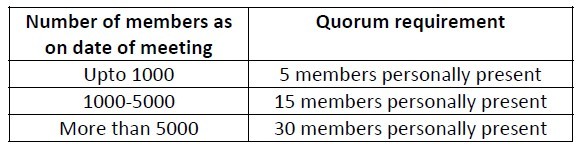

8. Quorum for public companies [Section 103]

9. Proxy:

• In case of companies formed not for profit, a member only can act as proxy for another member.

• No person shall act as proxy on behalf of members not exceeding 50 and holding in the aggregate not more than 10% of the total share capital of the company carrying voting rights.

• Restriction that unless the articles otherwise provide a member of a private company shall not be entitled to appoint more than one proxy to attend on the same occasion has been removed.

10. Voting through electronic means

Every listed company or a company having 1000 or more shareholders shall provide to its members facility to exercise their right to vote at general meetings by electronic means. [Section 108]

11. Postal Ballot

• No postal ballot for Ordinary business

• All items of business on which a director or auditor has right to be heard cannot be transacted through postal ballot.

• A brief report on the postal ballot conducted including the resolution proposed, the result of the voting thereon and the summary of the scrutinizer's report shall be entered in the minutes book of general meetings along with the date of such entry within thirty days from the date of passing of resolution.

• Following items of business can be transacted through postal ballot only, except in case of OPC and companies having less than 200 members:

a. Alteration of objects clause of MOA

b. Alteration of AOA by means of insertion or removal of provisions necessary to constitute a company as a private company in terms of Section 2(68)

c. Change of registered office outside the local limits of any city, town or village as specified in section 12(5).

d. Change in objects for which a company has raised money from public through prospectus and still has any unutilized amount out of the money so raised under section 13(8).

e. Issue of shares with differential rights as to voting or dividend or otherwise under Section 43(a)(ii)

f. Variation in the rights attached to a class of shares or debentures or other securities as specified under sec 48

g. Buy-back of shares by a company under section 68(1)

h. Election of a director under section 151

i. Sale of the whole or substantially the whole of an undertaking of a company as specified under sec 180(1)(a)

j. Giving loans or extending guarantee or providing security in excess of the limit prescribed under Sec 186(3).

Minutes

1. In case of Board and Committee meetings, the minutes shall also contain names of the directors present and names of directors who voted for and against each resolution.

2. Minutes shall not contain any matter which is defamatory to any person, is irrelevant or immaterial or detrimental to the interest of the company. Chairman to exercise discretion in this regard.

3. Secretarial Standards prescribed by ICSI to be observed in preparation of minutes.

4. A member who has made a request for provision of soft copy in respect of minutes of any previous general meetings held during a period of immediately preceding three financial years shall be entitled to be furnished, with the same free of cost.

|

CA SANJAY DEWAN

Major changes in Income Tax Returns for A.Y 2014-15

1. All taxpayers filing E-Returns will have to compulsorily update correct mobile number and E- Mail ID's. Otherwise there will be login issues before uploading of return on income tax Depts Website.

2. Now onwards Income Tax Refund will be issued directly in the bank account of the taxpayer through ECS only, cheques are discontinued. Therefore at most care should be taken while mentioning Bank Account Number and IFSC Code in the income tax returns.

3. From this year while claiming TDS in Income Tax return facility has been given to carry forward the TDS of previous year and brought forward TDS to next year. Due to this reconciliation of TDS claimed on Income and total available TDS as per Form 26 can be made. Tax payers which follow cash system of accounting will be benefited, like Doctors, Advocates, CAs and other professionals.

4. As per newly inserted Section 87A if annual income of the taxpayer is up to Rs. 5,00,000/- then Tax relief of maximum of Rs. 2,000/- is given. For claiming this relief separate space has been inserted in the return.

5. As per newly inserted Section 80EE if taxpayer has purchased house up to Rs. 40 Lakh and taken housing loan of Rs. 25 Lakh then taxpayer can claim deduction of interest up to Rs. 1 Lakh. For claiming this deduction separate space has been inserted in the return.

6. If income of the taxpayer is more than Rs. 1 crore then surcharge of 10% is applicable. For this separate space has been inserted in the return.

7. All salaries taxpayers will now have to give now separate details of LTA (Leave Travel Allowance) and HRA (House Rent Allowance) and other allowances separately. This will help Govt. to track proper claim of such deductions, recent HRA and LTA fallacious claimed by some MPs and Govt. taxpayers may have forced for such changes.

8. From this year the details of short and long term capital gain will have to be given in three parts viz.

a) sale of plot / flat

b) sale of STT paid shares and mutual funds

c) sale of other assets.

Further in case of sale of land or building Stamp Duty Value will have to be mentioned. Further if taxpayer is availing exemption under capital gains then value of newly purchased asset, date of acquisition of the asset and if invested in capital gain account then its details will have to be mentioned.

9. Corporate or LLP assessee will have to mention Corporate Identification Number or LLP Identification Number. Further Director or Designated Partner Identification Number will have to be mentioned. This will help in cross check of information with other legal departments by income tax dept or visa a versa.

10. If assessee carrying on business is taking deduction of bad debts of more than Rs. 1 Lakh of single person, then his PAN will have to be mentioned.

11. As per newly inserted section 43 CA if, taxpayer have sold other than capital assets below stamp duty value (eg. builders / developers) then the difference between the two will be considered as deemed income of the assessee and tax will have to be paid on it. For this separate space has been inserted in the return.

12. If there is more than one owner of the house then, while mentioning details in the schedule of Income from House Property the percentage of co ownership will have to be given.

13. From this year e-filing of wealth tax return is compulsory and in this return the details of all wealth whether taxable or not, will have to be given in depth.

.

.

|

CA SANJAY DEWAN

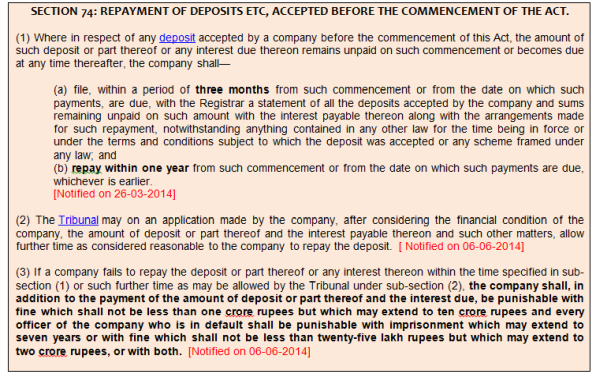

Filing of return of deposits in DPT-4

|

CA SANJAY DEWAN

Filing of Form MBP 1: Interest of directors

| Filing of Form MBP 1: Interest of directors |

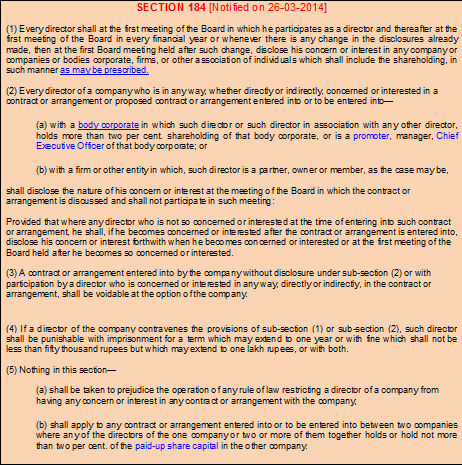

This is one of the important changes that have happened from Companies Act of 1956 (old act) to Companies Act of 2013 (new act). In the old act there was a requirement on the directors to disclose their interest to the company in form 24AA and the same needed to be taken on records by the company in a board meeting.

Similarly in the new act, a director has to disclose interest in form MBP 1 to the company in the first board meeting of the company. Section 184(1) and Rule 9(1) of Companies (Meetings of Board and its Powers) Rules,2014 deal with this requirement.

.png)

DUE DATE FOR FILING: Within 30 days of holding first Board Meeting.

SAVINGS FOR SMALL COMPANY: A Small Company need not get the same attested by a practicing professional, meaning the company can file the form itself.

PROCEDURE:

- Prepare MBP 1 in format notified by the government.

Download from

- Prepare board resolution

RESOLVED FURTHER THAT Mr. Mukesh Gupta, Managing Director of the Company, be and is hereby authorized to make necessary entries in the Registrar maintained for the purpose and to digitally sign and file E-form MGT.14 with the Registrar of Companies, NCT of Delhi and Haryana.

FURTHER RESOLVED THAT Mr. Aman Jain, Practicing Company Secretary, Kolkata be and is hereby authorized to certify and file Form MGT.14 with Registrar of Companies, NCT of Delhi and Haryana and to do such acts, deeds and things as may be considered necessary and appropriate to give effect to the above resolution."

- Take signatures on the above prepared forms and board resolution

- Scan the same and attach with Form MGT 14 and file the same with ROC.

Download form MGT 14 from the following link:

|

CA SANJAY DEWAN

Subscribe to:

Posts (Atom)